Two Big Headlines Shaking Up Homeownership

Two major housing headlines are making waves right now:

- Fannie Mae is removing its minimum credit score requirement for certain conventional loans.

- There’s a proposal for 50-year mortgages as a new affordability option.

At first glance, both sound controversial — and it’s true, the online chatter is mostly negative. But in real estate, every change brings both challenges and opportunities. Let’s take a look at how savvy buyers might actually benefit from these shifts.

Fannie Mae’s Credit Score Change

Starting November 16, 2025, Fannie Mae will no longer require a minimum 620 credit score for loans processed through its Desktop Underwriter (DU) system. Instead, the system will evaluate borrowers based on their overall financial profile—think income, assets, debt, and even rental payment history.

- The upside: This opens doors for borrowers with limited or “thin” credit histories—like recent graduates, immigrants, or those who prefer to live debt-free. If you’ve always paid your rent on time and managed your finances responsibly, you could now have a fairer shot at homeownership.

- The caution: Lenders will still be looking for financial stability. While the credit score barrier is coming down, responsible lending standards remain. It’s not a free-for-all, but it is a second chance for many who may have been overlooked.

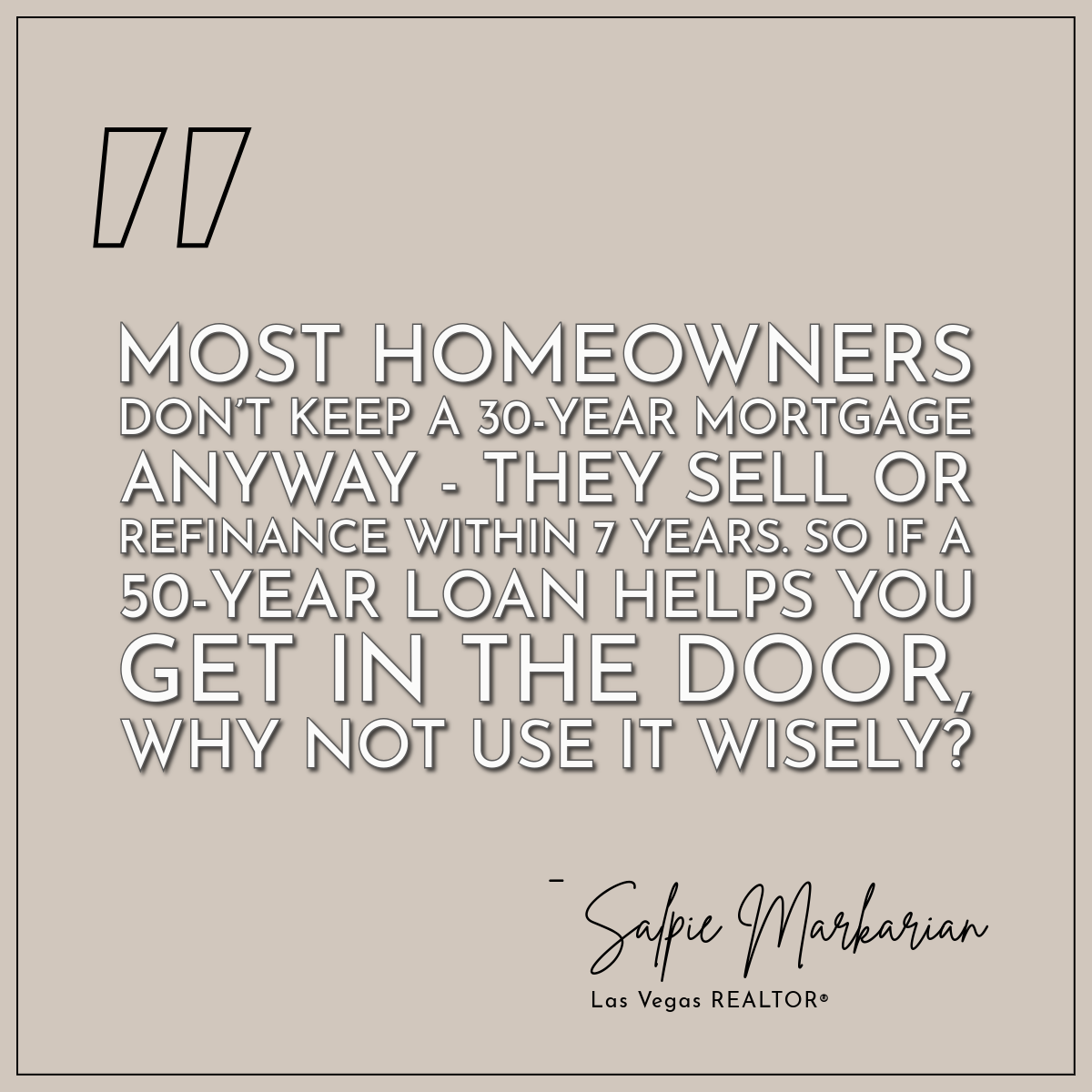

The 50-Year Mortgage Proposal

Talk of a 50-year mortgage might sound wild, but it’s being floated as a way to make monthly payments more affordable—especially in markets where prices have outpaced incomes. By stretching the loan over a longer period, buyers could see lower monthly costs, making homeownership more accessible.

- The upside: Lower monthly payments mean more people can afford to buy sooner, instead of waiting years to “save more” while prices and rents rise.

- The tradeoff: You’ll pay more total interest over time and build equity slower. It’s not ideal for someone planning to stay long-term — but for buyers who plan to refinance or sell in 5–10 years, it could be a smart short-term play.

How Smart Buyers Can Use This to Their Advantage

Here’s how to make these changes work for you, not against you:

- Get in the door sooner. These shifts could make qualifying easier or lower your monthly payment enough to finally move forward with homeownership.

- Be strategic. If you choose a 50-year term, use the monthly savings wisely — pay off high-interest debt, build your emergency fund, or invest in your future.

- Have a plan. Expect to refinance when rates drop or sell before the long-term costs add up. Flexibility is key.

- Work with pros. Partner with a lender and agent who understand these changes and can help you tailor the right move for your unique situation.

My Take

There’s a lot of fear online about these headlines, but I see opportunity — especially for first-time buyers who’ve been priced out or discouraged by credit score limits.

This isn’t about taking on more debt; it’s about being strategic. If these tools help you build equity instead of paying rent, that’s a win in my book.

In the end, it’s not about the system changing — it’s about how you play the game. With thoughtful planning and the right support, you can turn today’s market shifts into your advantage.

If you’re curious about how these changes might affect your path to homeownership, let’s connect! I’m here to help you navigate every step.

Thinking About Buying or Refinancing?

If you’re wondering how these updates might affect your next move — whether you’re a first-time buyer, an investor, or someone curious about refinancing — let’s chat.

I can connect you with my trusted mortgage partner who specializes in creative loan strategies (including VA and first-time programs) and help you see what’s actually possible in today’s market.

📩 Send me a quick message to get started.

Sources:

- Fannie Mae Announcement SEL-2025-09

- National Mortgage Professional – Industry reacts to 50-year mortgage idea

- AP News – 50-year mortgage proposal pros and cons

Categories

Recent Posts

Las Vegas Realtor® | License ID: S.0202353

+1(725) 277-0707 | sm@salpiemarkarian.com

GET MORE INFORMATION

The data relating to real estate for sale on this web site comes in part from the INTERNET DATA EXCHANGE (IDX) Program of the Las Vegas REALTORS®. Information deemed reliable but not guaranteed. © 2026 SALPIE MARKARIAN.